Do you think, all things being equal, a $2,000 stock is riskier than a $20 one?

This question arose from an argument I had with my dad: He never invested in stocks trading in the 1,000s because he claimed they tend to move in $100s almost daily, and preferred stocks trading at tens of dollars, as they only fluctuate by a few dollars (usually). Even when I pointed out that two hypothetical stocks, one trading at $2,000 and the other at $20, a $100 and $1 move, respectively, still only represent a 5% price change, he still insisted the former feels riskier than the latter.

This kind of reasoning made me wonder how prevalent it is among the general public, particularly among other retail investors. Such thinking could pose another problem for the efficient markets hypothesis and shed light on a lesser-known cognitive bias in the equities market: non-proportional reasoning. While this bias has been studied in psychology (Miller, Turnbull, and McFarland (1989), Kirkpatrick and Epstein (1992), and Yamagishi (1997)), the literature on how such reasoning shapes individual trading decisions in finance is limited. Shue and Townsend (2021) examine how non-proportional thinking affects the incorporation of news into stock prices, focusing on market-level outcomes such as volatility and beta. Whereas Birru and Baolian (2016) used option market data to conclude that investors care about nominal price and overestimate the skewness of low-priced stocks.

In contrast, this paper examines people’s decision to hold or sell their shares in a stock by treating them as price takers who react to stock-related news. In other words, instead of studying price formation as previous research has done, I focus on people’s reactions to observed losses in a price-taking environment, which more closely reflects the decision context faced by retail investors. After all, we have all woken up to see the Dow Jones Industrial Average fall by 1,000s of points, sometimes without a clear reason, and had to decide our next steps in the market that day.

This phenomenon might be more common in the US, where the media tends to focus on dollars rather than percent changes when reporting financial news. How often have we heard reports of the Dow Jones price change being reported in points instead of percent?

To investigate this cognitive bias, I ran a survey in which participants evaluated identical percentage price drops presented in different dollar terms. I then asked whether they would sell their shares and, if so, how many. The goal here was to see whether people attribute dollar changes to risk, so that the higher the nominal price change – even when the percentage change is identical – the riskier the stock appears and the more likely they are to react accordingly by selling more during a market downturn.

Since the underlying loss was identical across all questionnaires, any difference in behavior reflects how people interpreted the dollar amount of the price change.

Since the only difference among the questionnaires was the stock price and number of shares, the participants’ reactions should be similar, so that, under the assumption of a rational investor, for example, a $2,000 stock shouldn’t be considered riskier and sold more than a $2 stock.

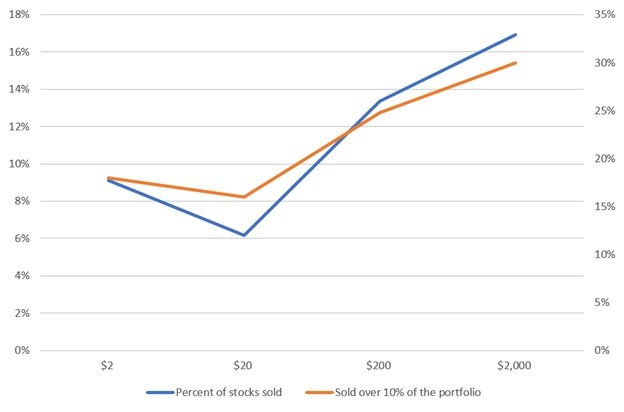

The raw results indicate significant differences, as shown in Figure 1. Specifically, the differences between lower-priced and higher-priced stocks were noticeable, as more people sold larger shares of their holdings due to the market crash. For example, among participants who faced the $2,000 stock, nearly 17% sold some or all their stocks, and the average portfolio sold was 30%; whereas, for the $2 stock, only 18% sold any shares, and the average portfolio sold was 9%. Hence, participants reacted more strongly to the $2,000 than to the $2 and wanted to hold less of the former.

Figure 1: Average percent of stocks sold in portfolio (left axis) and percent of people who sold their portfolio

Source: Survey of 632 American Adults

The pattern remains even after accounting for age, income, gender, and trading behavior. For every tenfold increase in stock price, the share of the portfolio sold rose by about 4 percentage points, the percentage of participants who sold any shares increased by 42%, and perceived risk increased by 17%.

The results suggest that people attribute a nominal price to a stock’s riskiness when evaluating it. In addition, participants who habitually follow stock-related news were more likely to exhibit non-proportional thinking, suggesting that such news may exacerbate this cognitive bias.

This finding sheds some light on another aspect of financial markets’ inefficiency and another cognitive bias that may hinder it. The ramifications of this study could indicate that media coverage in the US that focuses on dollar changes rather than percent change has made the problem worse. So perhaps the next time you hear about how the Dow Jones sheds 2,000 points or your stock in your 401 (k) portfolio fell by 50 points, you’d stop to consider whether that means a lot, given how small it is in percentage terms.

References

Birru, J., and Baolian, W. (2016). Nominal Price Illusion. Journal of Financial Economics 119 (3): 578–598

Kirkpatrick, L. A., and Epstein, S. (1992). Cognitive-experiential self-theory and subjective probability: further evidence for two conceptual systems. Journal of personality and social psychology, 63(4), 534.

Miller, D. T., Turnbull, W., and McFarland, C. (1989). When a coincidence is suspicious: The role of mental simulation. Journal of Personality and Social Psychology, 57(4), 581.

Shue, K., and Townsend, R. R. (2021). Can the Market Multiply and Divide? Non‐Proportional Thinking in Financial Markets. The Journal of Finance.

Yamagishi, K. (1997). When a 12.86% mortality is more dangerous than 24.14%: Implications for risk communication. Applied Cognitive Psychology: The Official Journal of the Society for Applied Research in Memory and Cognition, 11(6), 495-506.

This article draws on my academic research titled: Cents and Sensibility: Exploring Non-Proportional Reasoning During Stock Market Declines.